Jobboy

Jobboy

Introduction to Deferred Compensation in 2026

Deferred compensation represents a powerful component of total compensation beyond base salary, allowing mid-career professionals to build long-term wealth strategically. In 2026, understanding plans such as 401(k)s, pensions, and restricted stock units (RSUs) is essential when evaluating job offers or negotiating packages. These tools help optimize taxes, align incentives with company performance, and secure financial futures amid evolving market conditions. Mid-career individuals often face critical decisions about balancing immediate cash needs with future security, and deferred elements frequently determine which offer delivers superior lifetime value.

This guide provides a comprehensive framework for evaluating deferred compensation options, complete with real-world examples from finance and healthcare sectors, step-by-step decision processes, and practical negotiation language. We will also examine common pitfalls and how to structure conversations that highlight deferred benefits without appearing overly focused on pay alone.

Understanding Key Types of Deferred Compensation

Deferred compensation defers a portion of earnings to a future date, often with tax advantages. Common vehicles include employer-sponsored retirement accounts and equity grants. Each type carries distinct rules, contribution limits, and risk profiles that professionals must weigh carefully against personal circumstances and career timelines.

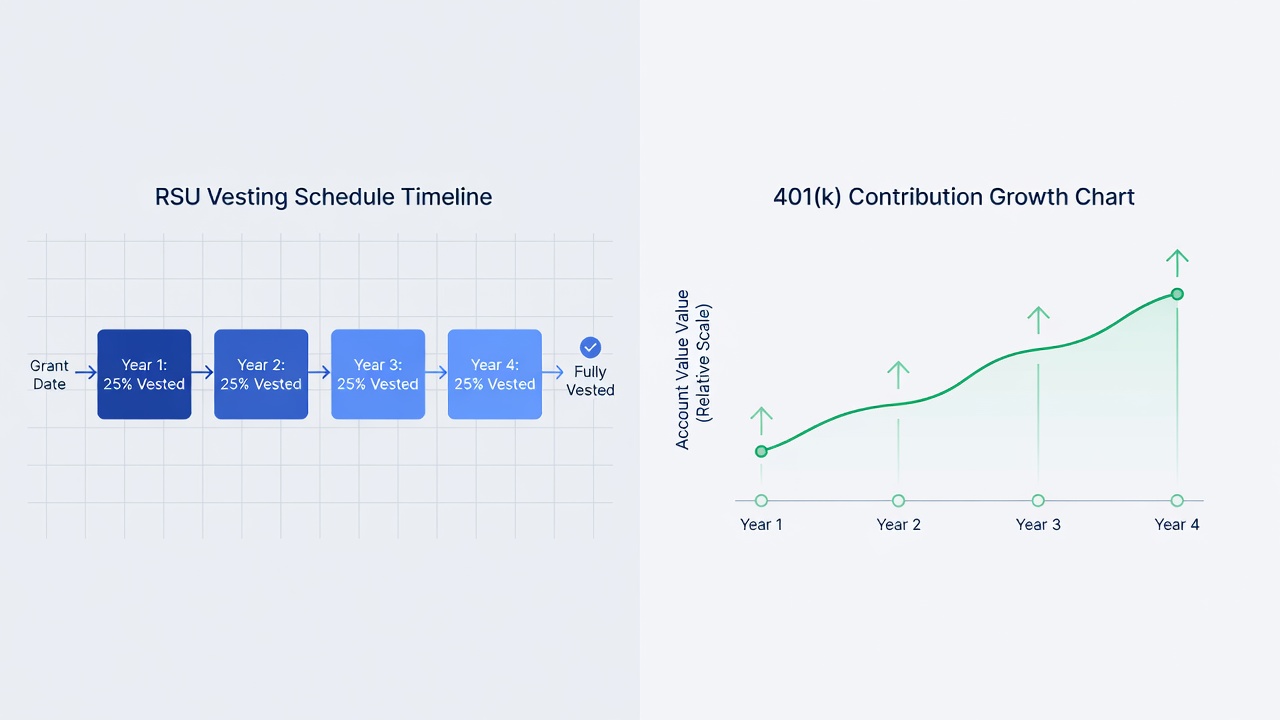

401(k) Plans and Similar Retirement Vehicles

Traditional and Roth 401(k)s remain foundational. Contributions reduce taxable income in the year made, with growth occurring tax-deferred until withdrawal. Many employers match contributions up to a percentage of salary, effectively providing free money when maximized. In addition to standard 401(k)s, some organizations offer 403(b) or 457 plans for nonprofit and public-sector roles, each with slightly different eligibility and withdrawal rules. Professionals should review whether catch-up contributions become available after age 50 and how automatic enrollment features affect their savings rate over time.

Pensions and Defined Benefit Plans

Traditional pensions promise a fixed monthly benefit based on salary and years of service. Though less common in private industry, they persist in government, healthcare, and certain finance roles, offering predictable income streams in retirement. Defined benefit formulas often incorporate final average pay multiplied by a service credit percentage, creating strong incentives to remain with one employer for extended periods. Hybrid cash-balance pensions combine features of both defined benefit and defined contribution plans, providing more transparency while still guaranteeing minimum returns.

Restricted Stock Units (RSUs)

RSUs grant employees company shares that vest over time. They tie personal wealth to organizational success but carry market volatility risks. Vesting typically occurs over three to four years with a one-year cliff. Some companies supplement RSUs with performance stock units that require specific financial targets to be met before any shares are released, adding an additional layer of complexity and potential upside.

Tax Implications of Deferred Compensation

Tax treatment varies significantly by plan type. Traditional 401(k) contributions lower current taxable income, while Roth options provide tax-free qualified withdrawals. RSUs are taxed as ordinary income upon vesting, regardless of whether shares are sold. Pensions receive favorable treatment as ordinary income upon receipt. Professionals should consult current IRS guidelines at IRS.gov when modeling scenarios. Additional considerations include the impact of the net investment income tax on large RSU vestings and how required minimum distributions from retirement accounts interact with other income sources later in life.

Vesting Schedules and Their Impact

Vesting determines when employees gain full ownership. Graded vesting spreads ownership gradually, while cliff vesting requires a set period before any ownership transfers. Early departure can result in forfeiture of unvested amounts, underscoring the importance of reviewing schedules before accepting offers. Some employers now offer accelerated vesting upon retirement or disability, and professionals negotiating packages should request written clarification on these provisions. Understanding how vesting interacts with company change-of-control clauses is equally critical, as mergers frequently trigger full acceleration that can dramatically alter personal financial planning.

Evaluating Risks of Early Withdrawal

Accessing funds before age 59½ typically triggers income taxes plus a 10% penalty on most retirement accounts. RSU sales before vesting completion are impossible, and pension commutations often reduce lifetime benefits. Consider liquidity needs and emergency funds separately from deferred plans. Certain exceptions exist for hardship withdrawals or substantially equal periodic payments, yet these carry long-term consequences that require careful modeling. Professionals should also evaluate the opportunity cost of lost compounding when funds are removed prematurely.

Step-by-Step Framework for Comparing Plans Across Offers

- Calculate total potential value including employer matches and projected equity growth, incorporating conservative and optimistic market assumptions.

- Assess vesting timelines against your expected tenure and any anticipated life events such as relocation or family changes.

- Model tax scenarios using current brackets and future projections, factoring in state tax differences if offers span multiple jurisdictions.

- Factor in company stability and industry outlook, reviewing recent earnings reports and analyst commentary for the organizations involved.

- Compare portability if career mobility is a priority, noting which plans allow direct rollovers or continued participation after separation.

- Review survivor benefits and spousal consent requirements, especially when pensions or large RSU grants are involved.

Real-World Examples from Finance and Healthcare

A mid-level investment banker at a bulge-bracket firm might receive substantial annual RSUs vesting over four years alongside a generous 401(k) match. In contrast, a healthcare administrator at a large hospital system could benefit from a defined benefit pension accruing a fixed percentage of final average salary per year of service plus a modest 401(k). A third scenario involves a senior consultant at a Big Four accounting firm who receives a combination of cash bonuses, RSUs, and eligibility for a supplemental executive retirement plan that provides additional income after age 60. These structures highlight how sector norms influence optimal choices and why professionals must look beyond headline compensation figures.

Negotiation Scripts for Incorporating Deferred Compensation

When discussing offers, use phrases such as: “I’m excited about the role and would like to explore how we might enhance the deferred compensation component, perhaps by accelerating RSU vesting or increasing the 401(k) match.” Another effective approach: “Given my long-term commitment, could we discuss pension eligibility or additional equity grants to align our mutual goals?” Follow up by asking for a side-by-side comparison of total rewards, including projected values over five and ten years. Always document verbal commitments in writing and request plan summaries before signing any offer letter.

Common Pitfalls and How to Avoid Them

- Ignoring the interaction between multiple plans, such as how pension benefits may be offset by Social Security at SSA.gov.

- Overvaluing equity grants without stress-testing against stock price declines or dilution events.

- Failing to review plan documents for early termination clauses or blackout periods that restrict transactions.

- Assuming all 401(k) matches are immediately vested, when many use a graduated schedule.

Frequently Asked Questions

What happens to unvested RSUs if I leave the company?

Typically forfeited, though some plans allow acceleration upon termination without cause or during a change of control.

Can I roll over a pension into an IRA?

Many plans permit lump-sum distributions that can be rolled over, but this eliminates guaranteed lifetime income and requires careful tax planning at DOL.gov.

How do I compare RSU value against a pension?

Project both over a 10- to 20-year horizon using conservative growth assumptions and discount rates, then adjust for risk tolerance.

Are there limits on how much I can defer annually?

Yes, IRS contribution limits apply to 401(k)s and similar plans, while RSUs are governed by company grant policies and securities regulations.

Should I prioritize a pension or a larger 401(k) match?

Evaluate based on expected tenure, desire for guaranteed income versus investment control, and overall retirement timeline.

Conclusion

Deferred compensation offers substantial wealth-building potential when evaluated thoroughly. By applying structured frameworks, understanding tax and vesting nuances, and negotiating confidently, mid-career professionals can maximize these elements within their total compensation packages in 2026 and beyond. Always review details with a qualified financial advisor tailored to your situation and revisit your strategy annually as life circumstances evolve.

No comments yet. Be the first!