Jobboy

Jobboy

Introduction to Remote Retirement Planning

Freelancers and digital nomads often face unique challenges when planning for retirement due to irregular income streams and international lifestyles. In 2026, remote retirement planning requires adaptable strategies that account for cross-border tax rules, variable earnings, and the need for portable financial tools. This guide provides actionable steps to help you achieve financial independence while working remotely. Many freelancers earn through platforms that pay irregularly, making traditional employer-sponsored plans unavailable. Instead, self-directed options become essential. Understanding how to integrate retirement savings into a nomadic routine can prevent future shortfalls and provide peace of mind during years of travel and project-based work.

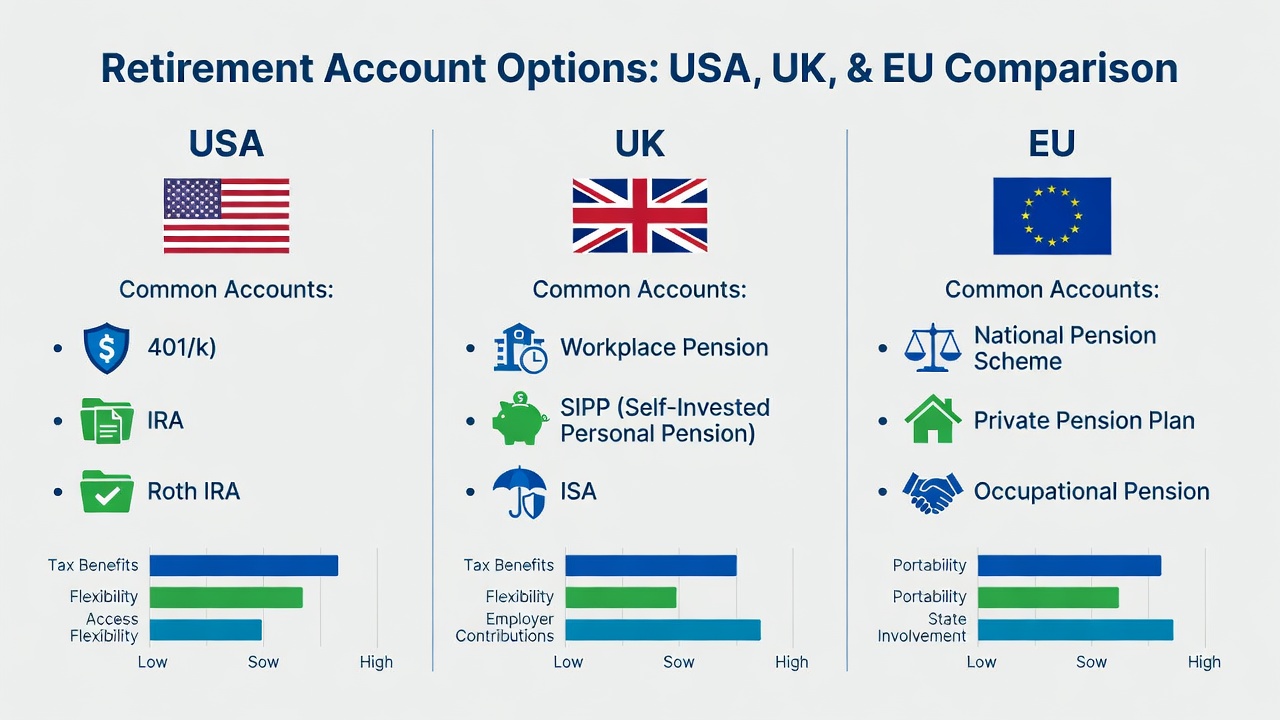

Retirement Account Options Across Borders

Choosing the right retirement vehicles is essential for long-term security. U.S.-based freelancers might start with a Solo 401(k) or SEP IRA, while those abroad can explore equivalents like the UK's SIPP or Singapore's SRS. Always verify eligibility based on residency and tax treaties. For example, a freelancer living in Thailand may still contribute to a U.S. IRA if they maintain U.S. citizenship, but they must navigate foreign earned income exclusions. Contribution limits adjust annually, and rules for early withdrawals vary widely. A cross-border tax advisor can help structure accounts to minimize double taxation and maximize growth. Digital nomads often maintain multiple accounts across jurisdictions to hedge against political or currency risks in any single country.

Diversified Investment Approaches for Irregular Income

With gig-based earnings, diversification across stocks, bonds, real estate, and index funds reduces risk. Dollar-cost averaging into low-cost ETFs provides stability despite fluctuating cash flow. Rebalance portfolios quarterly to maintain target allocations. Freelancers should also consider alternative assets such as peer-to-peer lending or dividend-paying stocks that generate passive income. Robo-advisors simplify the process for nomads on the move by automatically adjusting risk levels based on life changes. One practical example involves allocating 60 percent to global equities, 25 percent to bonds, and 15 percent to real estate investment trusts, adjusting as income stabilizes over time.

Building Emergency Funds While Traveling

Maintain 6-12 months of expenses in liquid, accessible accounts like high-yield savings or money market funds. Use multi-currency accounts to manage currency fluctuations during international travel. Track expenses meticulously with apps that support multiple currencies. Automate transfers to emergency reserves on high-income months. Keep funds in FDIC-insured institutions where possible. Nomads often split emergency reserves across two or three banks in different countries to protect against localized banking issues. Reviewing these funds every quarter ensures they remain aligned with changing living costs in new destinations.

Real-World Case Studies of Successful Nomad Retirees

Consider the example of a graphic designer who retired at 48 after consistently funding a Roth IRA and investing in global index funds over 15 years. She maintained a disciplined 25 percent savings rate even during low-earning months by drawing from a separate business operating account. Another case involves a software developer who leveraged a combination of U.S. and EU accounts to minimize taxes while living in Portugal under the Non-Habitual Resident regime. His strategy included quarterly tax estimates and automated contributions that adapted to project-based income spikes. A third freelancer, a content creator based in Bali, built a diversified portfolio including rental properties in two countries, allowing her to generate steady retirement income without selling assets prematurely.

Step-by-Step Checklists for Automating Savings

- Calculate your average monthly income over the past year using accounting software.

- Set up automatic transfers to retirement accounts on payday or immediately after invoice payments clear.

- Review and adjust contribution percentages every six months based on income trends.

- Integrate tax-advantaged accounts into your overall plan by linking them to your primary banking app.

- Schedule annual reviews with a financial advisor familiar with international tax rules.

- Document all contributions and projected growth to stay motivated during lean periods.

Comparison of Global Retirement Options

| Country/Region | Account Type | Key Benefit | Tax Advantage |

|---|---|---|---|

| United States | Solo 401(k) | High contribution limits | Tax-deferred growth |

| United Kingdom | SIPP | Flexible investments | Tax relief on contributions |

| European Union | Private Pension | Portability across borders | Varies by member state |

| Singapore | SRS | Tax-deferred contributions | Withdrawals taxed at lower rates |

Comparing Platforms That Offer Retirement Benefits

Several freelance marketplaces now integrate retirement features such as automatic contributions or matched savings. Evaluate options based on fees, ease of international access, and integration with banking tools. Official guidance from the IRS helps U.S. freelancers understand account rules, while the Social Security Administration details benefits for self-employed workers. Additional resources from the U.S. Department of the Treasury cover international tax treaties that affect retirement withdrawals.

Tax-Efficient Withdrawal Plans

Structure withdrawals to stay in lower tax brackets by spreading distributions over multiple years. Roth conversions during low-income years can reduce future liabilities. Factor in required minimum distributions if applicable and coordinate with Social Security timing. Freelancers should also maintain taxable brokerage accounts for flexible access without penalties, using them to bridge gaps before traditional retirement age. Monitoring tax law changes annually prevents surprises during withdrawal phases.

Common Mistakes to Avoid

Many freelancers overlook currency conversion fees when moving funds internationally, which can erode returns over decades. Another frequent error is failing to update beneficiary designations after relocating to a new country. Ignoring tax filing deadlines in multiple jurisdictions often leads to penalties that compound quickly. Finally, underestimating healthcare costs in retirement can derail even well-funded plans, so incorporating long-term care insurance early is wise.

FAQ on Common Pitfalls

What if my income varies wildly year to year?

Base contributions on a rolling average and maintain flexible accounts that allow catch-up contributions during strong years.

How do I handle taxes when moving countries?

Research tax treaties and consider becoming a tax resident in a favorable jurisdiction. Professional advice is critical to avoid compliance issues.

Are there penalties for early withdrawals?

Yes, many accounts impose penalties before age 59½. Plan liquidity through taxable brokerage accounts instead to avoid unnecessary costs.

Can I contribute to multiple retirement accounts simultaneously?

Yes, but total contributions across all accounts are subject to annual limits set by each country. Track them carefully to stay compliant.

Conclusion

Remote retirement planning empowers freelancers to secure their future despite non-traditional careers. Start with small, consistent actions today to build lasting financial security and enjoy the freedom of location-independent work for years to come.

No comments yet. Be the first!